Bankroll Management for Horse Racing: The Maths Behind Survival

Best Horse Racing Betting Sites – Bet on Horse Racing in 2026

Loading...

Bankroll Management for Horse Racing: The Maths Behind Survival

The uncomfortable truth about horse racing is that most people who bet on it lose money. Not because they are stupid, not because the sport is rigged, but because they treat betting as entertainment rather than as a discipline that requires structure, rules and — above all — arithmetic. Bankroll management for horse racing is not a glamorous subject. There are no hero stories here, no tales of a single inspired punt that changed everything. This is about the quiet, unglamorous work of protecting your capital so that the good selections you do make can compound over time rather than being wiped out by a chaotic week.

Consider the industry context. Total online betting turnover on British horse racing reached £8.73 billion in the 2023–2024 financial year, according to Gambling Commission data, a figure that had fallen 16.3% from the £10 billion recorded just two years earlier. That decline is partly structural — affordability checks and regulatory tightening have pushed some volume to unlicensed operators — but it also reflects a maturing market in which casual money is leaving and the remaining pool is increasingly informed. Competing in that environment without a bankroll framework is like entering a poker tournament without counting your chips.

This article sets out a practical bankroll management system designed for bettors who focus on all-weather racing, where the fixture density — over 200 meetings across six tracks each season — provides both opportunity and the potential for rapid capital erosion if stakes are uncontrolled. The principles apply to any form of horse racing, but the examples and seasonal structure are tailored to the all-weather calendar.

A note on scope: this is not about how to pick winners. Selection methodology is a separate discipline entirely. Bankroll management assumes you already have a method — good, bad or mediocre — and addresses the question of how to deploy your capital so that the method has the best possible chance of producing a profit over time. The best selection process in the world will fail if it is paired with chaotic staking. Conversely, even a modest edge can grind out a profit over hundreds of bets if the staking is disciplined and the bankroll is protected.

Why 90% of Racing Bettors Lose — and What the Top 1% Do Differently

The statistic is stark. Research by the National Centre for Social Research found that the top 1% of horse racing bettors — approximately 60,000 individuals — generate 52% of all betting revenue on horse racing. The implication is that a tiny fraction of the betting population is responsible for over half the money the industry takes in, and the vast majority of the remaining 99% are, collectively, net losers. That does not mean every individual in the 99% loses every year, but the structural economics are clear: without an edge and without discipline, the house wins.

What separates that top 1%? It is not secret information or insider tips. It is process. Professional and semi-professional bettors manage their bankroll with the same rigour that a fund manager applies to a portfolio. They define a starting bank. They set maximum stake sizes as a fixed percentage of that bank. They track every bet — winner and loser — in a spreadsheet or database. They review their performance over rolling periods. And they never, under any circumstances, chase a losing day by increasing stakes beyond their predetermined limits.

The scale of the industry’s take is captured neatly by the levy figures. “Levy yield for the 12 months to 31 March 2025 reached almost £109m, the fourth successive year of increase” — Alan Delmonte, Chief Executive, Horserace Betting Levy Board. That rising levy — calculated as a percentage of bookmakers’ gross profits — confirms that the bookmaking industry continues to profit handsomely from horse racing bettors. Your job, as a bettor with a bankroll management framework, is to ensure you are not contributing more than necessary to that total.

The psychological component is at least as important as the mathematical one. Most bettors who blow their bank do not do so because of consistently poor selections. They do so because of one catastrophic session where frustration, overconfidence or alcohol drove them to stake wildly beyond their normal parameters. A bankroll framework is, fundamentally, a defence against your worst self. It forces rational behaviour when emotion is screaming at you to double down.

Level Stakes, Percentage Stakes and the Kelly Criterion

The three most commonly discussed staking plans in horse racing are level stakes, percentage stakes and the Kelly Criterion. Each has strengths and weaknesses, and the right choice depends on your betting style, risk tolerance and the accuracy of your probability assessments.

Level stakes is the simplest approach: you bet the same fixed amount on every selection, regardless of the odds or your confidence level. If your standard stake is £10, every bet is £10 — a 6/4 favourite and a 20/1 outsider receive the same commitment. The advantage of level stakes is clarity. There is no calculation required, no temptation to inflate stakes on “certainties” and no complicated adjustment when the bankroll fluctuates. The disadvantage is inefficiency: you are allocating the same capital to high-confidence selections as to speculative ones, which means your best bets are under-staked and your weakest bets are over-staked relative to their expected value.

Percentage stakes addresses that inefficiency partially. Instead of a fixed pound amount, you bet a fixed percentage of your current bankroll — typically 1% to 3% per bet. As the bankroll grows, your stakes grow proportionally; as it shrinks, stakes reduce automatically. This creates a natural brake during losing runs and accelerates compounding during winning periods. The practical challenge is discipline: when your bankroll is depleted and your standard 2% stake has shrunk from £20 to £12, the temptation to override the system and bet more is considerable. Do not. The system works precisely because it scales down when you are losing.

The Kelly Criterion is the mathematically optimal staking plan, developed by John Kelly at Bell Labs in 1956. It calculates the ideal stake as a function of your edge (the difference between your estimated probability and the implied probability of the odds) divided by the odds minus one. In theory, Kelly maximises long-term growth of the bankroll. In practice, it requires you to estimate the true probability of each outcome with a degree of accuracy that few bettors possess. Overestimate your edge by even a small margin and full Kelly will push you to dangerously large stakes. Most professional bettors who use Kelly operate on a fractional basis — typically quarter-Kelly or half-Kelly — which sacrifices some theoretical growth in exchange for significantly reduced variance.

For all-weather racing bettors, percentage stakes is usually the most practical choice. The high fixture volume means you are placing bets frequently — potentially several times a week — and the automatic scaling of percentage stakes keeps your exposure proportionate to your capital at all times. Level stakes works well for recreational bettors who want simplicity and are not concerned with maximising growth. Full Kelly is a tool for specialists with proven, quantified edges and the emotional control to withstand the swings it produces.

Whichever plan you choose, the cardinal rule is the same: never stake more than 5% of your bankroll on a single bet. At 5%, a run of five consecutive losers — which happens far more often than most people expect — reduces your bankroll by roughly 23%. At 10% per bet, that same losing run costs you 41%. The maths is unforgiving, and it does not care about your gut feeling.

Seasonal Allocation: Splitting Your Bankroll Across the AW Calendar

All-weather racing runs year-round, but the volume of fixtures and the quality of betting opportunities fluctuate with the seasons. The core all-weather season runs from October through April, when turf courses are dormant and the synthetic tracks host the majority of British flat racing. During this period, fixture density peaks — Southwell, Wolverhampton and Newcastle may each race two or three times a week — and the volume of data available for analysis is at its highest.

The Gambling Commission’s participation data illustrates the seasonal dynamic from the demand side. Horse racing betting participation among UK adults rose from 4% in the January-to-April 2025 window to 7% in the April-to-July 2025 period — a three-percentage-point jump that coincides with the start of the turf flat season and major festival meetings. That spike in participation means more money in the market during spring and summer, but most of it flows towards turf racing. All-weather markets during these months can become even thinner than usual, as both casual bettors and professional attention shift to the prestige turf programme.

The HBLB Annual Report for 2024–2025 recorded that levy yield reached a record £108.9 million, the fourth consecutive year of growth. That headline number masks the underlying turnover decline per race. The money flowing into racing is generating more profit for bookmakers relative to turnover — which means the average bettor is getting a worse deal. A seasonal allocation strategy accounts for this by concentrating activity during periods when your analysis is strongest and the data most abundant, rather than betting uniformly across the year.

A practical allocation might look like this: assign 60% of your annual bankroll to the core winter all-weather season (October to April), 25% to the shoulder months (August, September, May) and 15% to the summer months when all-weather fixture density drops and your attention may be split with turf racing. This is a guideline, not a rigid formula — adjust it based on your own track record and the volume of opportunities you identify. The principle is to match your capital deployment to the periods where your edge is largest.

Dealing With Losing Runs: Variance Is Not Failure

Every bettor, no matter how skilled, will experience losing runs. This is not a possibility; it is a mathematical certainty. If you back horses at an average price of 4/1 with a genuine 25% strike rate — which would represent a profitable long-term edge — you will still encounter stretches of ten, fifteen or even twenty consecutive losers. That is what variance looks like at those odds. The question is not whether losing runs will happen, but whether your bankroll and your psychology can survive them.

The maths is instructive. At a 25% strike rate, the probability of losing ten bets in a row is roughly 5.6%. Over the course of 500 bets in a season — a reasonable number for an active all-weather bettor — a ten-bet losing streak is more likely than not to occur at least once. At a 20% strike rate (typical of longer-priced selections), the probability of a ten-bet losing run is 10.7%, and a fifteen-bet losing streak has around a 3.5% chance. These are not fringe events. They are routine features of a betting landscape dominated by uncertainty.

The danger of losing runs is not financial — provided your staking is controlled. It is psychological. After a dozen consecutive losers, even disciplined bettors begin to doubt their method. They start second-guessing selections, abandoning rules that have served them well, or — worst of all — increasing stakes to try to recover losses quickly. This is the point where bankroll management earns its keep. If your staking plan says 2% per bet and your bankroll has shrunk by 20%, your stake has reduced automatically. The system is doing its job. Trust it.

One useful exercise is to simulate losing runs before they happen. Take your staking plan, your current bankroll and your average strike rate, and calculate how many consecutive losers you can absorb before the bankroll drops below a level you consider critical. If that number feels uncomfortably small, your stakes are too high. Adjust before the losing run arrives, not during it. Preparation eliminates panic. Panic eliminates bankrolls.

There is also a seasonal dimension to variance in all-weather racing. The winter months, when fixture volume is highest and you may be betting three or four times a week, compress the variance into shorter timeframes. A ten-bet losing streak that might take a month to accumulate during the quieter summer period can unfold in a single week during a busy January. The emotional intensity of a fast-moving losing run is greater, even though the mathematical implications are identical. Being prepared for that tempo — and having rules that prevent impulsive reactions — is part of the framework.

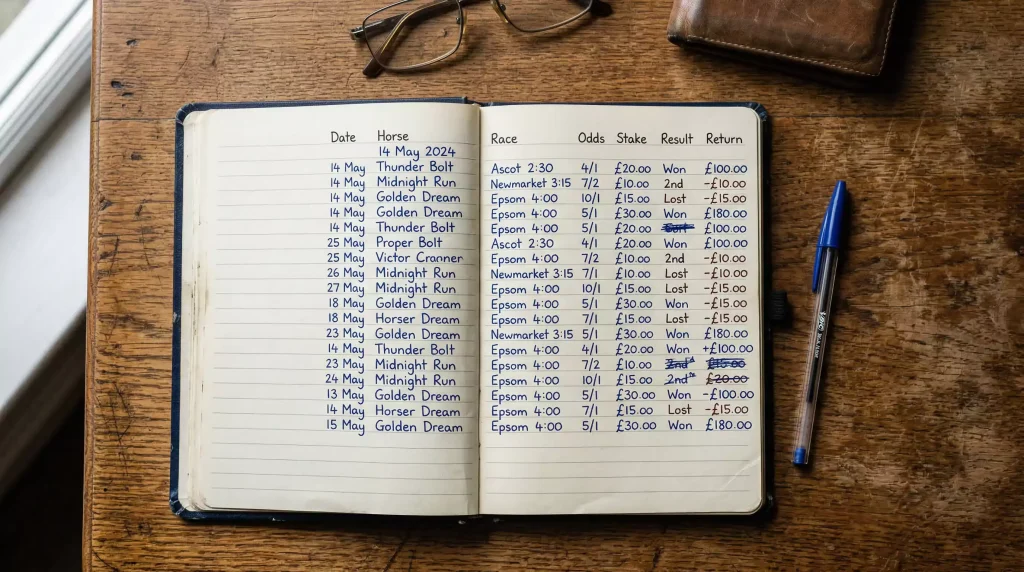

Recording and Reviewing Every Bet

If you are not recording your bets, you are not managing your bankroll. You are guessing. A betting record does not need to be elaborate — a simple spreadsheet will do — but it needs to capture enough information to allow meaningful review. At a minimum, log the date, course, race type, horse name, odds taken, stake, result and profit or loss. For all-weather bettors, adding columns for surface type, field size and the primary reason for the selection (draw, pace, class drop, trainer form) turns a raw record into an analytical tool.

The purpose of recording is not to catalogue wins and feel good about them. It is to identify patterns in your losses. Are you losing disproportionately on certain race types? At certain courses? With certain trainers? At certain odds ranges? These patterns are invisible without data but glaringly obvious once you sort a spreadsheet by category. A bettor who discovers they are profitable on handicaps at Southwell but unprofitable on maidens can immediately cut out the losing category and improve their overall return without changing anything else about their approach.

Review frequency matters. Checking your record daily is counterproductive — the sample is too small to draw conclusions, and a bad day will skew your perception. Monthly reviews are more useful. Compare the month’s results against your long-term averages. Has your strike rate held up? Have the odds you are taking shifted? Is the ratio of winners to losers consistent with your expected edge, or has something changed? If the underlying method is sound but the short-term results are poor, that is variance. If the method itself has stopped working — perhaps the trainers you follow have changed their approach, or a surface resurfacing has altered form — that requires a strategic adjustment.

Quarterly reviews are where the bigger picture emerges. Over three months and 100-plus bets, you have enough data to evaluate whether your bankroll management horse racing approach is genuinely profitable or merely surviving on a lucky streak. Calculate your return on investment as a percentage: total profit divided by total stakes. For context, professional horse racing bettors typically aim for an ROI of 5% to 10% over a season. Anything above 10% sustained over hundreds of bets is exceptional. If your ROI is negative after a full quarter, the honest response is to reduce stakes, review your selection methodology and consider whether the time invested justifies the results.

When to Withdraw Profits and When to Reinvest

A bankroll that only grows and never pays out is not a bankroll — it is a number on a screen. One of the least discussed aspects of bankroll management is the withdrawal strategy: when to take money out, how much to take and how to prevent withdrawals from undermining the growth of the fund.

The simplest rule is a threshold-based approach. Set a target — say, 50% growth on your starting bank. When the bankroll reaches that threshold, withdraw a portion of the profit and reset the working bank to a slightly higher base. For example, if you started with £1,000 and the bankroll reaches £1,500, withdraw £300 and continue with a new base of £1,200. The withdrawal rewards your discipline and converts paper profit into real money. The reinvested portion gives the bankroll room to grow further while retaining a buffer above the original starting point.

The danger of never withdrawing is that it obscures the purpose of the exercise. Bettors who continually reinvest all profits can find themselves with a large notional bankroll that they have never actually used — and when a bad spell inevitably arrives, the unrealised profit evaporates. Taking regular, structured withdrawals forces you to crystallise gains and provides a tangible return on the time and effort invested. It also recalibrates your psychology: a withdrawal reminds you that the bankroll is real money, not Monopoly currency.

Conversely, withdrawing too aggressively stunts growth. If you strip out every penny of profit the moment it appears, the bankroll never compounds. A useful guideline is to withdraw no more than half of any profit that exceeds your target threshold, leaving the other half to increase the working base. Over time, this approach produces a steadily rising bankroll and a series of periodic payouts that reward your efforts without cannibalising the fund.

One final point: keep your betting bankroll entirely separate from your personal finances. A dedicated betting account — ideally with a separate bank card — prevents the temptation to dip into household money during a losing run and stops betting profits from being absorbed into everyday spending without being noticed. Bankroll management for horse racing only works if the bankroll is a defined, isolated entity with its own rules. The moment it bleeds into your general finances, the discipline collapses and the system ceases to function.